Estimated Tax Payments for Individuals in 2026

Federal and California estimated tax rules differ in the places that create the most avoidable mistakes: thresholds, safe harbors, and California’s front-loaded 30%, 40%, 0%, and 30% payment pattern.

For many individuals, estimated tax issues start when income changes but withholding does not. A side business grows, a larger K-1 arrives, investments are sold, or retirement distributions begin without enough tax being withheld. The money comes in, but the tax never gets prepaid.

The direct answer: if your income is not fully covered by withholding, estimated tax payments may be required. For 2026, the general federal threshold is whether you expect to owe at least $1,000 after withholding and refundable credits. California generally starts at $500, or $250 if married filing separately. In both systems, the real goal is usually not perfect forecasting. It is paying enough, on time, to stay inside the safe-harbor rules and avoid underpayment penalties.

If income is coming in through self-employment, K-1s, investments, rentals, or retirement distributions, estimated tax usually needs a mid-year review. For 2026, the next standard federal and California due date after spring filing season is June 15, 2026.

Who usually needs estimated tax payments

Estimated tax payments most often affect people whose income is not fully covered by employer withholding. That commonly includes:

- self-employed individuals and independent contractors

- partners and S corporation shareholders with pass-through income, including owners reviewing entity structure and single-member LLC tax benefits in California

- landlords and investors, especially those also evaluating moves like cost segregation for rental properties

- retirees taking distributions with little or no withholding

- individuals with significant capital gains, dividends, or interest income

The issue is not whether you have a complicated return. The issue is whether enough tax is being prepaid during the year.

The core federal and California rules for 2026

The general federal rule is that you usually need estimated tax payments if both of these are true:

- you expect to owe at least $1,000 after subtracting withholding and refundable credits

- your withholding and refundable credits will be less than the smaller of 90% of your 2026 tax or 100% of your 2025 tax

If your 2025 AGI was over $150,000, or over $75,000 if married filing separately, the federal prior-year safe harbor usually becomes 110% of your 2025 tax instead of 100%.

California follows the same idea, but not the same mechanics. California generally requires estimated payments for 2026 if:

- you expect to owe at least $500, or $250 if married filing separately, after withholding and credits

- your withholding and credits will be less than the smaller of 90% of your 2026 California tax or 100% of your 2025 California tax

For higher-income California taxpayers, the prior-year rule usually becomes 110% once 2025 California AGI is over $150,000, or over $75,000 if married filing separately. If 2026 California AGI is at least $1,000,000, or $500,000 if married filing separately, California requires the estimate to be based on current-year tax.

There is also a California-only surcharge that is easy to leave out of the estimate. California adds a 1% tax on taxable income above $1,000,000 (the Mental Health Services Tax, now part of the Behavioral Health Services Act), and the FTB expects that 1% to be built into your estimated tax. A taxpayer who crosses $1,000,000 of California taxable income and estimates only the regular brackets will be short by 1% of the amount over that line, on top of everything else.

That safe-harbor point matters more than many people realize. In many cases, the planning question is not “Can I estimate my exact 2026 liability perfectly?” It is “What amount do I need to prepay to avoid a penalty while the year is still moving?”

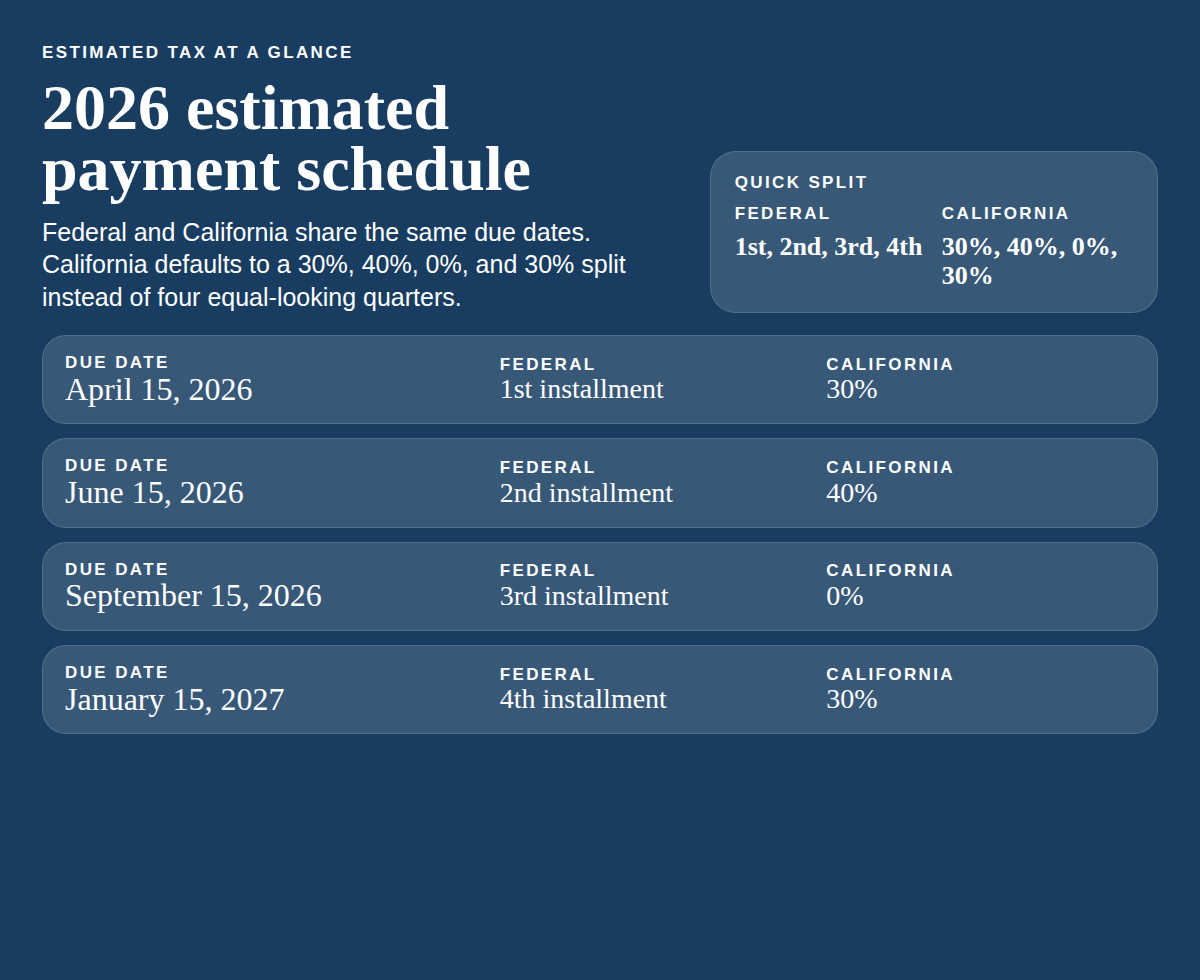

2026 estimated payment schedule

Federal and California estimated payments use the same four due dates: April 15, June 15, and September 15, 2026, plus January 15, 2027. The big difference is the California default split of 30%, 40%, 0%, and 30% rather than four equal quarters.

Timing problems, clean fixes, and common mistakes

If income is uneven, equal payments are not always the right answer. The annualized income installment method can sometimes reduce or eliminate penalties by matching the required payment more closely to when the income was actually earned. The annualized method is reported on Form 2210, Schedule AI for federal, and on FTB Form 5805 for California. Both require period-by-period income records, so it only pays off when the income really was bunched into the later part of the year.

Estimated payments are also not the only fix. In many households, stronger withholding is cleaner than separate vouchers, especially when the problem is found mid-year or one spouse still has W-2 wages. For many households, withholding is easier to manage than separate quarterly payments, especially when the income mix changes midstream. If you also have business income, our post on the Orange County small business tax checklist for 2026 covers the broader planning side.

Most avoidable penalties come from a few repeat mistakes:

- relying on last year’s payment amount even though income increased materially

- assuming California installments should be four equal quarters

- missing estimated tax on K-1 income, capital gains, or retirement income

- waiting until year-end instead of recalculating mid-year

- focusing only on the federal estimate and forgetting the California one

When income changes during the year, the estimate usually needs to change with it.

If you want to know whether your current withholding and estimated payments are enough, Bharmal can project the federal and California numbers before the next deadline and help you adjust the plan without guessing. Schedule a conversation.